PFL doesn't use your salary

Most people assume EDD takes their current salary, multiplies by 70%, and that's the benefit. It doesn't work that way.

EDD looks backwards in time at a specific 12-month window called the "base period." They pull your W-2 wages from that window, find the quarter where you earned the most, and calculate your benefit from that one quarter. Your current salary doesn't matter. Your offer letter doesn't matter. Only the wages your employer actually reported to EDD during the base period quarters.

What the base period is

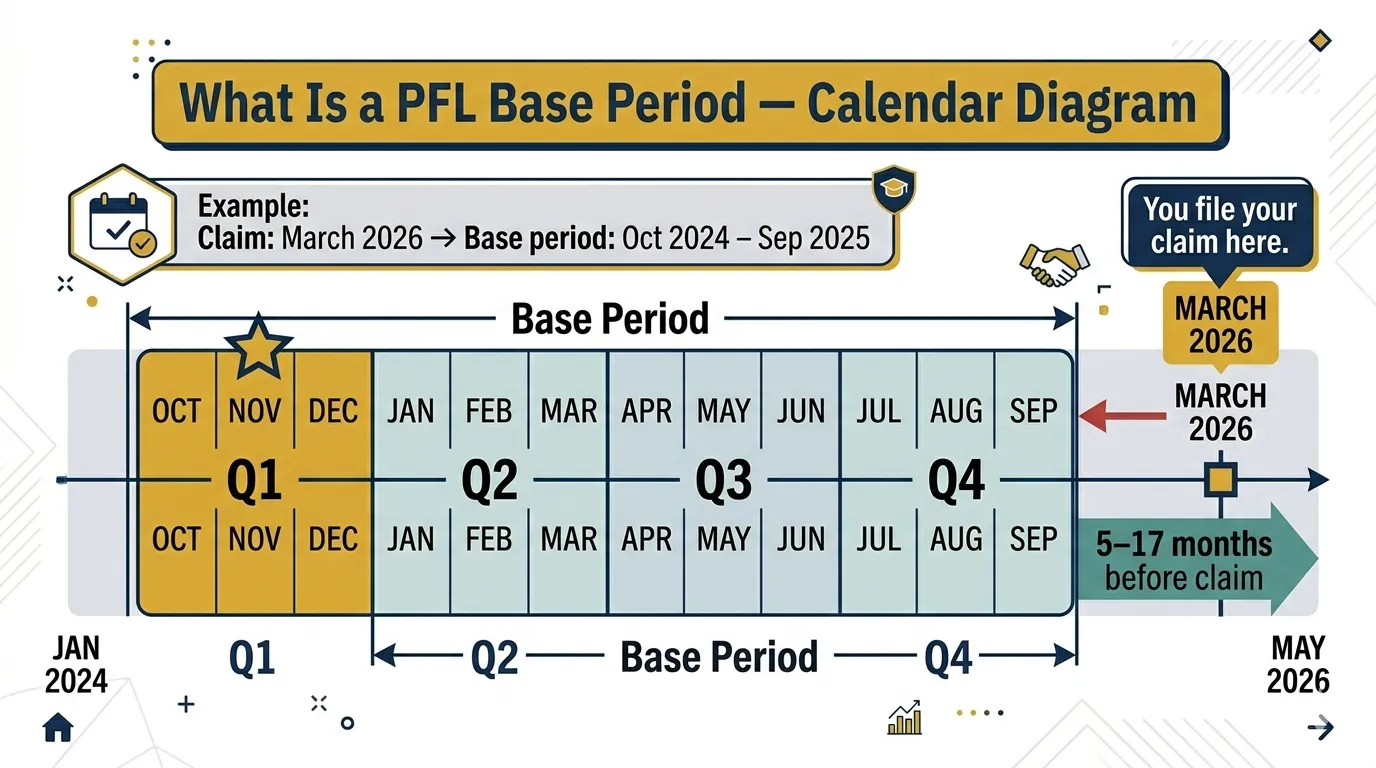

Example: claim filed March 2026 → base period is Oct 2024–Sep 2025

The base period is 12 months long and is divided into four calendar quarters. It does not start from your claim date. It starts from 5 to 18 months before your claim, depending on which month you file.

California uses fixed calendar quarters: Jan-Mar, Apr-Jun, Jul-Sep, Oct-Dec. Your claim start date determines which four quarters make up your base period. The lag exists because EDD needs time to receive and process the quarterly wage reports from employers.

Here's the part that confuses people: there's a gap between the end of the base period and your claim date. That gap is at least one full quarter, sometimes two. Wages earned during that gap don't count.

How to find your base period

EDD publishes a table, but it's easier to just look at when your claim starts:

| If your claim starts in | Your base period is | Gap (wages not counted) |

|---|---|---|

| January, February, or March 2026 | Oct 2024 - Sep 2025 | Oct-Dec 2025 |

| April, May, or June 2026 | Jan 2025 - Dec 2025 | Jan-Mar 2026 |

| July, August, or September 2026 | Apr 2025 - Mar 2026 | Apr-Jun 2026 |

| October, November, or December 2026 | Jul 2025 - Jun 2026 | Jul-Sep 2026 |

Notice the pattern: the base period always ends one full quarter before your claim quarter. If you file in May 2026 (Q2), the base period runs through December 2025 (end of Q4 2025). Everything you earned from January 2026 through May 2026 is invisible to the calculation.

Three examples with different claim dates

Example 1: Steady salary, no surprises

Maria earns $80,000/year and files PFL in April 2026. Her base period is Jan 2025 to Dec 2025. Each quarter she earned $20,000. Highest quarter: $20,000. AWW: $20,000 / 13 = $1,538. Benefit: $1,538 x 70% = $1,077/week.

This matches what our calculator would show for an $80,000 salary. No surprises because her income was steady throughout the base period.

Example 2: the raise that doesn't count

Say you earned $60,000 through all of 2025, then got bumped to $85,000 on January 1, 2026. You file PFL in May. Your base period? Jan 2025 through Dec 2025. The entire time you were at $60,000.

EDD sees $15,000 per quarter. Your benefit comes out to $808/week. Meanwhile your coworker who's been at $85,000 all along gets $1,154/week for the same leave. The difference over 8 weeks is $2,769. That's the cost of the base period lag.

What happens with commission income

Commission workers and sales reps tend to have wildly uneven quarters. Suppose someone closed a big deal in Q3 2025 and earned $28,000 that quarter, while Q1 was $12,000, Q2 was $14,000, and Q4 was $11,000. Total income: $65,000.

If EDD divided annual income evenly, each quarter would be $16,250 and the weekly benefit would be $875. But EDD doesn't average. They take the best quarter. $28,000 / 13 = $2,154 AWW. At 70%, that's $1,508/week. Nearly double what an even-split calculation would give.

The flip side: if your best quarter was Q1 and you had a bad year after that, the highest-quarter method still picks Q1. Uneven income can work for you or against you depending on which quarter was strongest.

The highest quarter method

Once EDD has your four base period quarters, the rest is mechanical. They take the single quarter with the most reported wages. Divide by 13. That gives them your average weekly wage. Then they apply 70% (or 90% if the AWW is $1,252 or below).

They do not average all four quarters. They do not look at total annual wages. Only the best quarter. This is actually generous compared to some states, which use multi-quarter averages.

What goes into a quarter's total: regular wages, overtime pay, bonuses paid during that quarter, commissions paid during that quarter, vacation pay that was cashed out. What doesn't count: tips that weren't reported to EDD, severance pay, stock options or RSU vesting (unless processed as W-2 wages in that quarter), 1099 contractor income.

When the base period works against you

You just started a new job

If you switched jobs 3 months ago, your base period might contain wages from your old, lower-paying job and zero from your current one. Or worse, if you had a gap between jobs, one or more quarters might show zero wages.

You went from full-time to part-time (or vice versa)

The base period locks in wages from 5-18 months ago. If you were part-time then and full-time now, your benefit will reflect the part-time wages. The reverse is also true: if you were full-time last year and cut to part-time recently, the base period actually helps you since it uses the higher wages.

You were unemployed for part of the base period

Unemployment benefits are not wages. If you were on UI for one or two quarters of your base period, those quarters will show $0 or very low wages. EDD still picks the highest quarter, so having one or two bad quarters doesn't necessarily destroy your benefit, as long as at least one quarter had decent wages.

You do need at least $300 in total base period wages to qualify for PFL at all.

You work two jobs and only one withholds SDI

If your second job pays you as a 1099 contractor, those wages won't appear in your base period at all. Only W-2 wages where SDI was withheld get reported to EDD. This is common with people who have a main W-2 job and do freelance work on the side. The freelance income is invisible to the PFL calculation.

The alternate base period

If the standard base period gives you a low benefit (or makes you ineligible), California has an alternate base period. It uses the four most recent completed quarters before your claim. The difference is small but can help in specific situations.

The alternate base period matters most when you had very low or no wages in the standard base period but earned more in the quarters immediately before your claim. EDD is supposed to check both base periods and use whichever gives you a higher benefit, but in practice you may need to ask.

How to check your actual wages before filing

This is the most useful thing you can do before filing a PFL claim. Log into myEDD and look at your wage history. It shows the quarterly wages your employer reported. If there's an error (your employer underreported, or a bonus was attributed to the wrong quarter), you need to catch it before you file, not after.

If the numbers look wrong, contact your employer's payroll department first. They file corrections through their quarterly tax returns to EDD. Getting a wage correction after you've filed a claim is much harder and can delay your benefits by weeks.

If you're planning leave several months from now, remember that a different claim month can shift your base period. Run the numbers for each possible start month and see which gives you the best highest quarter. This is especially relevant for people with uneven income, like commission workers, freelancers who also have W-2 work, or anyone who changed jobs in the last year.

Not legal advice. Benefit estimates based on the EDD formula. Your actual PFL benefit is determined by EDD from official wage records. Source: EDD PFL benefit amounts, EDD base period chart.