Two rates, one formula

California PFL doesn't pay everyone the same percentage. Lower earners get 90% of their average weekly wage. Everyone else gets 70%. There's no sliding scale between them. It's one or the other.

Someone earning $24,000 a year can't absorb a 30% pay cut during family leave the way someone earning $100,000 can. California responded by setting a wage threshold and giving workers below it a better rate.

This has been the structure since 2018, when California switched from a flat 55% rate to the current two-tier system. The percentages have since been raised — in 2025, SB 951 increased the tiers from 60%–70% up to 70%–90%. But the formula's shape is the same: two rates, one cutoff.

The 2026 threshold: $1,252 AWW

In 2026, the $1,252 AWW threshold determines your rate — that's about $65,000 in annual salary

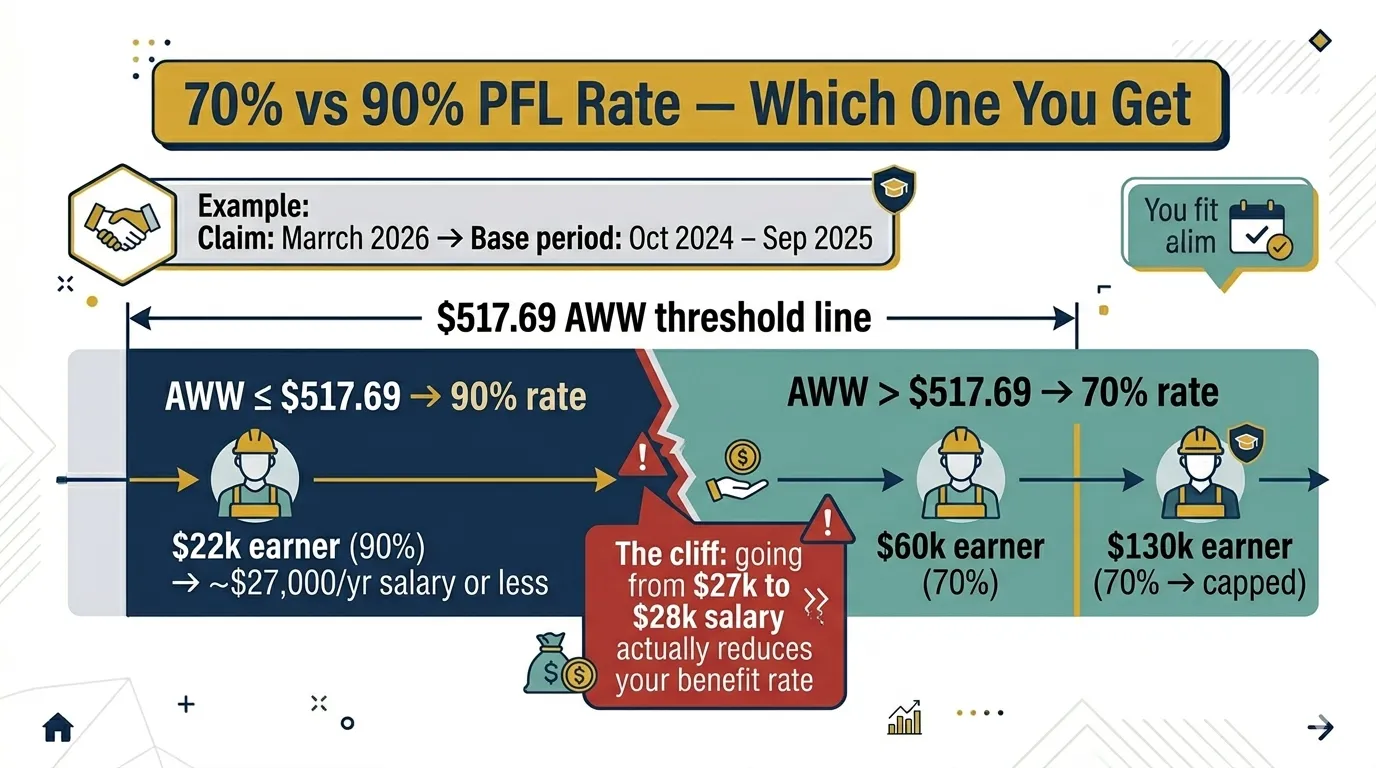

The dividing line is your average weekly wage (AWW), not your salary. If your AWW is $1,252 or less, you get 90%. If it's even one dollar more, you get 70%.

Your AWW comes from your highest-paid quarter in the base period, divided by 13 weeks. So the real question is: did your best quarter's earnings exceed $16,280 ($1,252 × 13)?

In annual salary terms, assuming even pay across quarters, $1,252 AWW works out to about $65,120 per year. But "assuming even pay" is doing a lot of work in that sentence. If you're a seasonal worker, a gig worker, or someone whose hours fluctuate, your actual AWW might land on either side of $1,252 regardless of what your annualized income looks like.

What changed from 2025 to 2026

The threshold isn't a fixed number. It's tied to the State Average Weekly Wage (SAWW), which California recalculates every year based on wage data reported to the Employment Development Department. The 90% tier applies when your highest quarter's wages are at or below 70% of the State Average Quarterly Wage.

In 2025, the SAWW was $740, putting the 90% threshold at $517.69 AWW (about $27,000 in annual terms). In 2026, the SAWW jumped to $1,789, and the threshold rose with it to $1,252.30 AWW (about $65,000 annual). That's a substantial shift — a worker earning $50,000 a year was a 70% earner in 2025 but is a 90% earner in 2026.

Four real salary examples

| Scenario | Best quarter | AWW | Rate | Weekly PFL |

|---|---|---|---|---|

| Cashier, $18/hr, 30 hrs/week | $7,020 | $540 | 90% | $486 |

| Part-time retail, $16/hr, 20 hrs/week | $4,160 | $320 | 90% | $288 |

| Teacher, $65,000/year | $16,250 | $1,250 | 90% | $1,125 |

| Software engineer, $140,000/year | $35,000 | $2,692 | 70% | $1,765 (cap) |

Three of these four workers get the 90% rate in 2026. That's a major change from 2025, when the cashier and the teacher would both have been on the 70% tier. The teacher at $65,000 is right at the edge — their AWW of $1,250 is barely under the $1,252 cutoff. A modest raise or some quarterly overtime could push them into the 70% tier next year, even if their cost of living hasn't changed.

The 90% rate isn't a windfall — it's a percentage of a smaller AWW. The part-time retail worker gets 90% but only $288/week, because the underlying wage is low. A higher percentage of a small number is still a small number.

The cliff at the threshold

There's something awkward about a hard cutoff at $1,252 AWW. Consider two workers:

Worker A has an AWW of $1,252. They get 90%, so $1,127 per week.

Worker B has an AWW of $1,253. They get 70%, so $877 per week.

One dollar more in AWW and the weekly benefit drops by $250. That's a real cliff.

In practice, this affects a narrow band of people right around $65,000 in annual salary (assuming even quarterly pay). If you're close to that line, it's worth checking your actual base period wages at myEDD. You can't choose which quarter EDD uses, but at least you'll know which side of the line you land on.

What counts as wages for the AWW calculation

EDD uses the wages your employer reported to them via quarterly tax filings (DE 9C). This includes your regular pay, overtime, bonuses, and commissions that were paid during the quarter. It does not include tips that weren't reported, under-the-table payments, or income from self-employment (unless you opted into SDI as a self-employed person).

Some specifics:

Bonuses can help. If you received a $5,000 bonus in Q2 and that pushed your Q2 wages above other quarters, EDD will use Q2 as your highest quarter. This can raise your AWW and your benefit.

Overtime counts too. Nurses, warehouse workers, and others who do regular overtime often have one quarter with significantly higher wages. EDD always picks the best quarter, so heavy overtime in one quarter helps you even if other quarters were lighter.

Multiple jobs are combined. If you worked two W-2 jobs simultaneously and both withheld SDI, the wages from both jobs go into the same quarter totals.

Common confusion with the rates

"I thought PFL pays 60%?"

It did, years ago. California went from a flat 55% rate to a two-tier system in 2018, then adjusted the percentages a couple more times. The short version: 60% hasn't been the rate since 2024. SB 951 took effect January 1, 2025, and the tiers became 90% for lower earners (AWW at or below the annual threshold — $1,252 in 2026) and 70% for everyone above that.

"Is my PFL benefit taxed?"

PFL is not subject to California state income tax. But it is taxable at the federal level. EDD sends you a 1099-G form. Plan for roughly 10-22% of your PFL benefit going to federal taxes, depending on your bracket. You can ask EDD to withhold federal taxes from your payments, or you can pay estimated taxes yourself.

"Does the rate apply to my salary or my AWW?"

Your AWW, not your salary. If you earn $80,000 a year, your AWW (assuming even pay) is $1,538. The benefit is $1,538 x 70% = $1,077 per week. It is not $80,000 x 70% / 52 weeks.

"Can I get both PFL and SDI at the same time?"

No. PFL and SDI are separate programs and you can only collect one at a time. But you can collect them back-to-back. A common sequence for new mothers: SDI during the pregnancy disability period (typically 6-8 weeks), then PFL for bonding (up to 8 weeks). Both use the same 70%/90% rate structure and the same benefit formula, so your weekly payment stays the same when you switch from SDI to PFL.

Estimates based on the EDD benefit formula. Not legal advice. Your actual benefit depends on your official wage records with EDD. Source: EDD PFL benefit calculation.